Fearless Growth, Relentless Execution

May Property Market Update

Summary

• House price inflation is running at -0.1% annually

• Is the general election going to affect the housing market?

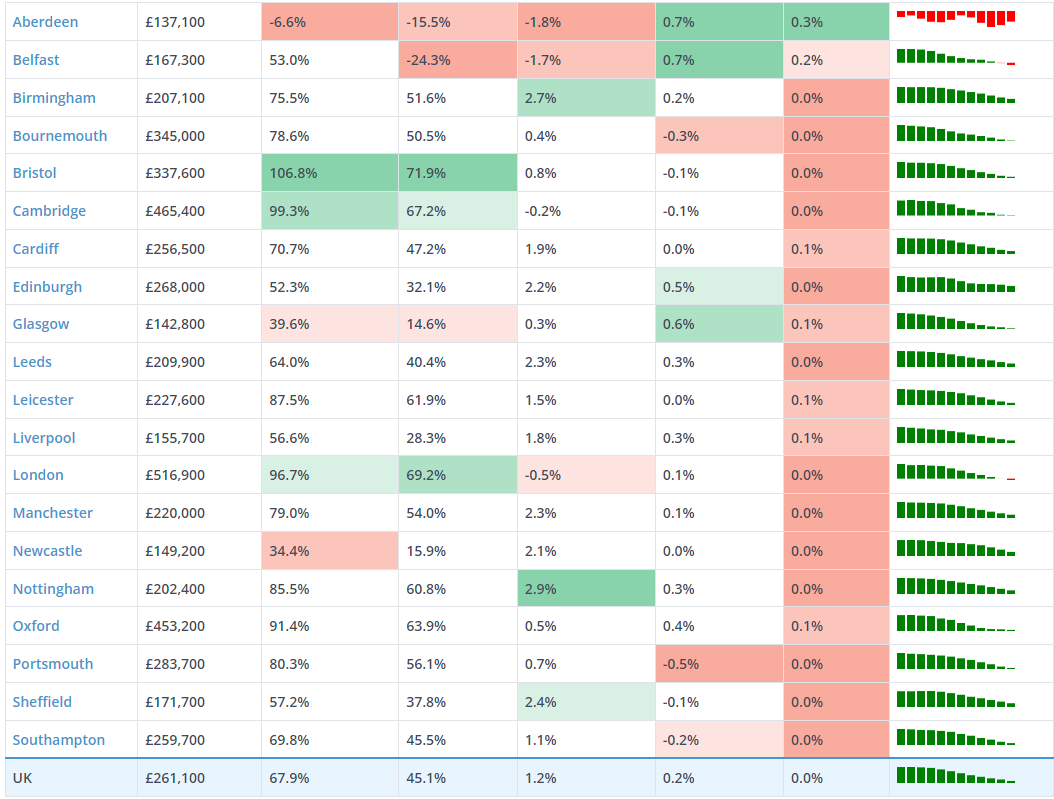

• At city level, price inflation ranges from -3% in Ipswich to +3.6% in Belfast – southern cities continue to register small price falls

• Sales activity up year-on-year by 13% with more sales agreed

• £230bn value of homes for sale, more than at any point in the last 8 years – up 20% year-on-year in number terms and 25% higher in value terms

• The north-south divide in pricing to remain with regards to inflation

• The general election is likely to stall the upward momentum in sales agreed

• +0.4% increase in house price inflation during April 2024

Increasing supply to keep house prices steady

The level of activity in the sales market is continually increasing. The number of sales agreed is higher year-on-year across all regions and countries of the UK. House prices are broadly static, falling 0.1% over the last 12 months. With the increase in supply it is likely to keep prices at a static level.

Impact from General Election?

Elections normally lead to increased uncertainty and some stalling in market activity.

There are currently 392,000 homes in the sales pipeline working their way through to completion over 2024. This is 3% higher than this time last year and it’s unlikely to see buyers already in the process of progressing to sales completions pulling out.

The demand to move remains for many households. In particular, first-time buyers, who are looking to escape the rapid growth in rents in the private rented sector. Similar is true of up-sizers, many of whom delayed moving last year when mortgage rates moved higher and now keen to go.

Realistically the election announcement is likely to stall the pace at which new sales are being agreed in the coming weeks, which is normal for the summer period typically anyway.

Those who are in the earlier stages of purchasing may look to delay decisions until the autumn after the election is over.

Overall, I don’t see the election having as big an impact as in previous years, particularly as there is not a huge divide in policy between the two main parties.

Other than a focus on reforming the private rental sector and boosting housing supply, there isn’t much being mooted on the housing side of politics. However, sales completions over 2024 may now fall slightly short of the 1.1m I expected for 2024.

What businesses and landlords will want to see from all political parties is specific plans for how we can boost housing supply across all tenures, while getting the right reforms into the private rented sector to ensure we maintain supply while giving renters more protections.

Highest amount of homes for sale in 8 years

With sellers returning to the market in growing numbers. The average agent has 31 homes for sale, up 20% on this time last year and the most in 8 years.

In value terms, there is £230bn of housing for sale, 25% higher than a year ago. This has grown largely due the increase of 3/4 bedroom homes being marketed, during the pandemic there was a chronic shortage of these, specifically during second half of 2023. During the second half of 2023 homeowners delayed moving, awaiting results of mortgage rates, house prices and buyer demand, once they realized all wasn’t so bad we have seen huge numbers come to market.

Most homes for sale are new-to-market. However, it is important to note that almost a third of homes currently available for sale (31%) were also listed for sale in 2023 but failed to find a buyer. This is not surprising, as demand for homes fell over the second half of the year as mortgage rates jumped higher.

Importantly 43% of these homes that had been on the market in 2023 have had their asking price cut by more than 5% to attract demand. This highlights the importance of pricing homes correctly at the outset, rather than aiming too high and not attracting buyers, your best chance to get the best money is in the first 10 weeks of marketing, so pricing correctly is imperative in the current market.

Sales on the UP

With there being more supply, that also means more buyers – seeing as most sellers are would-be buyers. In total we are 13% up year-on-year in sales agreed. Sales volumes are continuing to recover back towards the long-run average. Sales agreed have grown 22% across the North East but are up by just 1% in Wales.

The South West of England has recorded a 33% increase in homes for sale compared to last year, with an above-average increase in the expansion in 4-bed homes for sale. This is increasing a better supply and demand average for would-be buyers, compared to the shortage of options between 2020-2023.

Tax changes for holiday lets and the prospect of double council tax for second homes are likely to be encouraging some owners to sell. This exacerbates the expansion in homes for sale across the South West, which has the highest concentration of holiday homes. For me this isn’t a smart choice from the government and could have negative affects on the property markets in these areas specifically.

Increase in stock will keep house price inflation stagnant

The growth in available supply is welcome news, why? Because the lack of supply over recent years, pushed house prices to an over-inflated price-range. A return to greater availability will support the growth in sales.

However, I expect this expansion in supply to keep house price inflation in relatively stagnant for the remainder of 2024.

I stick to previous predictions, that I would imagine further (modest) decreases in areas across the south over the remainder of 2024.

Prices to continue falling across Southern England

Although the annual price of inflation has improved specifically over the last three months, there’s still a clear divide between Southern England and the rest of the UK, where houses have shown modest gains.

This is best demonstrated through a city-level view on annual house price inflation, which ranges from a low of -3% in Ipswich to a high of 3% in Belfast. There is a broadly equal split between cities with rising and falling house prices.

This is mainly due to house prices, increased mortgage rates and the ability to borrow larger mortgages. Coastal areas attracted an inflow of demand over the pandemic in the ‘Race for better lifestyle & space’ – are registering above-average price falls, as demand weakens, and these one-off pandemic factors fade. Remember, prices were pushed to over-valued areas due to the demand, I saw this first hand on countless occasions.

The current variation in house price inflation to continue over 2024 as incomes and house prices realign with the greatest adjustment across London and Southern England.

Want to learn more about property? I offer structured coaching & mentorship programes, alternatively you can invest WITH me. Drop me a message!

Check out the latest property index below:

All information is generated from personal knowledge of the current real estate market, rightmove, zoopla and hometrack.